We Compare 100's of loans from leading lenders

A HELOC is a type of loan that’s secured against your home. However, unlike many loans, the home equity line of credit gives you more control over how much you borrow, as you can draw out the money you need throughout the drawdown period.

Most HELOC agreements have a five-year drawdown faciality, and you’ll only make repayments on what you take out during this period. These loans are available to homeowners who have built up property equity.

Home equity lines of credit are mainly associated with the USA, but they recently became available for UK homeowners. Lenders and borrowers alike see the benefits of these products, including flexibility and the potential to save money.

We match our clients with lenders in the UK who offer these innovative borrowing solutions.

HELOCs enable homeowners to borrow against the equity they’ve built up. For example, if your home is worth £500,000 and your mortgage is £200,000, you could get a HELOC loan for up to £100,000. ( We can lend up to 85% of the property value with a maximum loan size of £250,000)

A lender will evaluate how much they’re willing to offer based on your equity and credit history, and household income, but HELOCs are secured against your property, which gives lenders more security.

In This Guide

Other Categories

While a home equity line of credit is secured against your home, it’s different to other secured loans When you take out a secured loan, you receive a lump sum and make monthly repayments on that amount – plus interest.

HELOCs have a pre-agreed amount, but you can borrow what you need for five years. During your draw period, you’ll only pay for the interest on what you borrow, but many people make principal repayments to reduce the cost of their line of credit.

Traditional secured loans have set repayment periods, but HELOCs offer more flexibility and can be easier to manage.

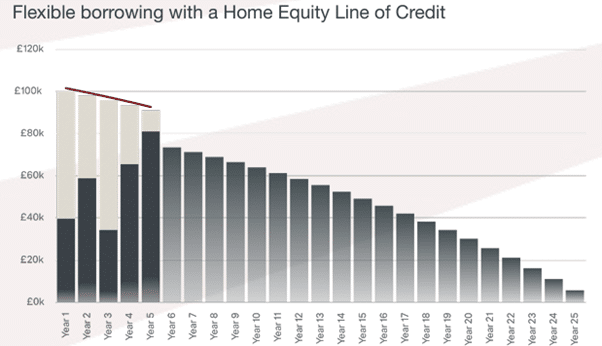

The HELOC products we offer typically have drawdown periods of five years, which means you can withdraw as much as you need from the agreed amount during this time.

For example, if you secure a HELOC for £100,000, you can take the money as needed over the first five years. You could take £40,000 in the first year and then £20,000 in the next year, repay £25,000 year 3, take another £40,000 in Year 4 and another £15,000 in year 5, at the end of the fifth year whatever your current balance is you repay the same way you would a standard loan. You will make payments during the 1st 5 year but based on the amount you have outstanding.

You will agree your loan term at the start of the application – for example a 25-year term (300 months) During the first 5 years you can use the drawdown facility, after 5 years your outstanding balance will switch to a standard term loan for the reaming 20yrs (240 months)

Standard secured loans are ideal for situations where all of the money is required day 1, such as debt consolidation, while HELOCs can help you with ongoing purchases like funding a home improvement project or business purposes.

For example, if you don’t know how much you’ll spend, you can save money with a line of credit, whereas traditional loan providers offer a one-off lump sum.

Sometimes, a HELOC might be the best solution for home improvements. If you’re adding an extension or remodelling your property, a line of credit can help you budget for the work, only spending what you need.

It also lets you plan the renovations on an ongoing basis rather than having to buy everything outright.

If you plan on private schooling, a HELOC loan might be beneficial, as it lets you pay the fees each term. Taking out a traditional loan means you’ll receive a lump sum for the fees, but your repayments will begin immediately.

When you choose a HELOC loan, you can withdraw money for each term and only pay interest on that amount. Simply put, there are fewer financial burdens with lines of credit.

Getting a quote won’t affect your credit score

Any financial product is a significant decision, and it’s essential to understand whether HELOCs are suitable for your financial goals. They come with a range of benefits, including:

While these agreements offer numerous benefits, there are also some things to consider before applying. The potential drawbacks of a HELOC include:

Your eligibility for these loans depends on a few factors. Before applying for one, your advisor will ask questions to assess whether you’re likely to be successful. The eligibility criteria include:

Only homeowners are eligible for these loans, so you’ll need to prove you have legal rights to a property. The amount of equity you’ve built up also matters, as the amount you can borrow depends on it.

For example, if you only have £10,000 worth of equity, lenders might not be willing to offer a HELOC. Most also specify a loan to value (LTV), a percentage of your equity. Securing a lower LTV rate will decrease your repayments and interest rates.

Lenders often use an applicant’s credit score to understand their borrowing history. A high score shows you’re responsible when borrowing money and making timely repayments, while lower scores present more risk to lenders.

While a less-than-excellent credit history won’t necessarily rule you out of a HELOC, it does mean the interest rates and repayments might not be as favourable.

Any loan means you must make repayments until it’s paid in full. HELOCs are more manageable for most people, but you’ll still need to consider whether you can manage repayments in the future.

Taking out a smaller amount and not using the entire line of credit can help you manage the loan more effectively.

We’re extremely proud to be rated ‘Excellent’ for our service standards. We’ve helped thousands of customers across the UK over the last 15 years to find the right finance for their needs – no matter how complicated the circumstances. And we look forward to helping you.

If you’d like to explore your HELOC options, our specialists can assess your eligibility and help you access the best rates for your needs. We work with clients from all backgrounds and have a network of dedicated lenders who judge your eligibility on an individual basis.

✔ Get unparalleled support from one of the UK’s leading secured loan brokers

✔ Find a HELOC provider that aligns with your needs and gives you favourable rates

✔ Discover your eligibility with no impact on your credit score

✔ We help you throughout the application process

There’s no time like the present for you to look forward to the future, and our dedicated brokers can help you find the right financial products. Please fill out the contact form, and we’ll get back to you.

You can also call us at: 01656 766 158

Our friendly team of brokers are on hand to answer any questions you have about flats and secured loans. You can get in touch with them today by calling 01656 766 158 and they’ll be more than happy to help.

If you have a question – we’d be happy to talk to you – simply call us…

(Mon-Fri 9am-8pm, Sat 10am-1pm)

Our Rating

At Willows Finance we ensure your personal information is kept secure and confidential.

PRIVACY OF YOUR INFORMATION

At Willows Finance Ltd, we appreciate that your privacy is extremely important to you. With this in mind, we have put in place a number of measures to ensure that any personal details we obtain from you as a result of visiting this website is processed and maintained in accordance with accepted principles of good information handling and also in accordance with the Data Protection Act 1988.

This statement provides you with details of the type of information we may hold about you, how we obtain and use information and how we protect your privacy.

Willows Finance Limited

Brocastle, Bridgend, CF35 5AS

Authorised and regulated by the Financial Conduct Authority

Firm Reference Number: 670052

Company Number: 6678545 (Registered in England and Wales)

This document outlines the services we provide. If you need clarification, please contact us at 01656 766158.

We offer first and second charge regulated mortgage contracts for business or personal use.

Other finance options may include:

Regulatory Status:

We offer an advised mortgage broking service and provide enough information for you to make an informed decision.

We are not independent financial advisers. Free debt advice is available from the Money Advice Service.

You can view our privacy policy at: https://willowsfinance.co.uk/privacy-cookie-policy/.

Lenders may also have their own privacy policies which will be provided to you.

We charge a broker fee upon loan completion. The average fee is approximately 5%, depending on your situation.

Fee details:

No refund is offered after completion. You may pay upfront or add the fee to your mortgage. Fees and commission will be detailed in your ESIS and Mortgage Agreement.

You will receive a Mortgage Agreement and an ESIS document detailing:

You may cancel your application anytime before completion without any charge. Mortgages cannot be cancelled after completion.

Missing payments can lead to charges, repossession, and negative impacts on your credit rating.

Consolidating debt may result in higher long-term interest. Securing debt against your home increases risk.

Your home may be repossessed if you do not keep up repayments on a mortgage or other loan secured on it.

If you wish to complain, contact us at:

Willows Finance Limited

Brocastle, Bridgend, CF35 5AS

Tel: 01656 766158

You may be able to refer your complaint to the Financial Ombudsman Service.

We are covered by the FSCS. You may be eligible for compensation of up to £85,000 per person per firm for mortgage advice and arranging.

More info: www.fscs.org.uk

After processing your application, you’ll receive a Mortgage Agreement and have a 7-day reflection period.

Contact us during this period with any questions. To proceed, sign and return the agreement.

Let us know what you're looking for today